Bitcoin's Golden Future

Could bitcoin be the next gold?The idea has a lot of intuitive appeal. Gold bugs and bitcoin fetishists tend to share a deep distrust of fiat currency and the nation state, an impregnable bullishness about their favored asset class, and an obsessive attention to details of market movements combined with a blithe disinterest in bigger-picture issues.The idea has become particularly popular as the value invested in bitcoin and other cryptocurrencies has marched upward over the past year. Even after this week's selloff, prompted by China declaring initial coin offerings illegal, the value of all cryptocurrencies in circulation is around $155 billion, according to Coinmarketcap.com.

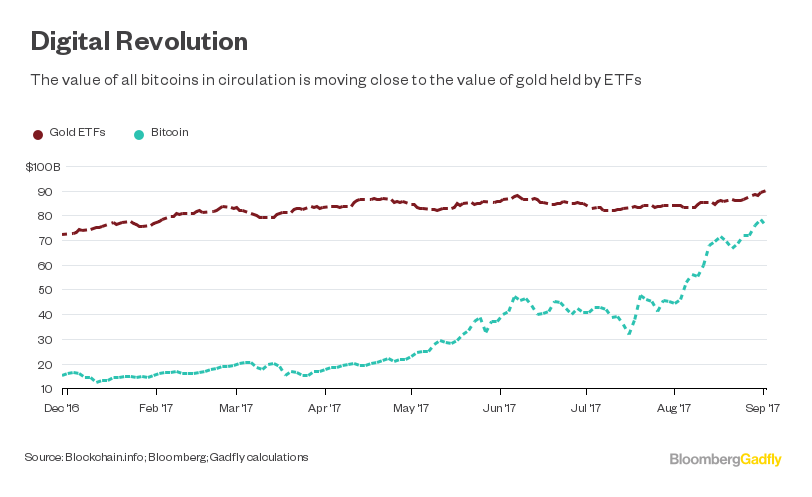

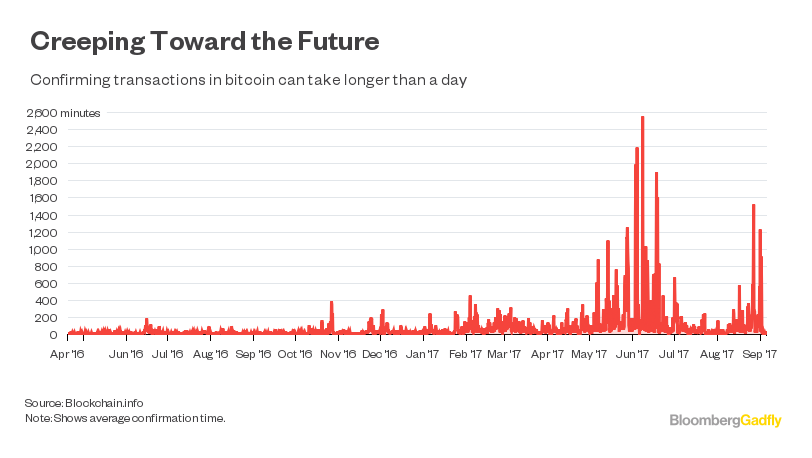

That may sound small compared to the $7.8 trillion notional value of the world's 187,200 metric tons of gold. At the same time, it's already about a tenth the value of the 40,000 tons of yellow metal used for investment as bullion bars and coins, and has overtaken the amount held in gold exchange-traded funds. At more than $78 billion, Bitcoin alone isn't far from overtaking the $90 billion-odd invested in all gold ETFs.There are two main reasons to doubt bitcoin's viability as an investment. One is an engineering issue: Its creaky infrastructure is likely to be a turn-off for all but the hobbyist fringe. Another is more philosophical: Digital currencies have no fundamental value, so have no place in a portfolio.Both objections are weaker than you might think.Take infrastructure. It's certainly true that bitcoin's operations are surprisingly clunky. Just confirming a single transaction typically takes more than an hour or longer — it briefly took more than a day at one point last month, according to software company Blockchain.info.

Having said that, financial markets are generally built on similar Rube Goldberg foundations. It's comically difficult for ordinary investors to buy an actual barrel of crude oil, as Tracy Alloway of Bloomberg News found out a few years back. The economist John Maynard Keynes, according to one possibly apocryphal story, once measured up the storage capacity of the chapel of King's College, Cambridge after coming perilously close to having to take delivery of a month's worth of the U.K.'s wheat supply. Completing transactions in the real world is often so clunky that some banks are already exploring using, um, blockchains instead.What makes markets investable for the most part is not their physical foundations, but the superstructure of derivatives contracts, exchanges and clearing houses built on top.To date, the world of bitcoin exchanges has been the wild west. When Mt. Gox filed for bankruptcy in 2014, it said it had lost 850,000 coins worth more than $450 million. Another $70 million-odd was stolen in a hack of Bitfinex last year. The likes of Deribit and Bitmex have been offering bitcoin futures and options for some time, but major institutional investors are only going to participate if they think the clearing and settlement process is rock-solid and the exchange itself reliably solvent.Change on that front is imminent. The Chicago Board Options Exchange is planning to start offering cash-settled bitcoin futures by next April, CNBC reported last week. Trading platform LedgerX LLC last month won regulatory approval from the U.S. Commodity Futures Trading Commission to act as a clearing house for derivatives settled in digital currencies. The ability to short or take leveraged positions in digital currencies could open them to a far wider array of investors.

Having said that, financial markets are generally built on similar Rube Goldberg foundations. It's comically difficult for ordinary investors to buy an actual barrel of crude oil, as Tracy Alloway of Bloomberg News found out a few years back. The economist John Maynard Keynes, according to one possibly apocryphal story, once measured up the storage capacity of the chapel of King's College, Cambridge after coming perilously close to having to take delivery of a month's worth of the U.K.'s wheat supply. Completing transactions in the real world is often so clunky that some banks are already exploring using, um, blockchains instead.What makes markets investable for the most part is not their physical foundations, but the superstructure of derivatives contracts, exchanges and clearing houses built on top.To date, the world of bitcoin exchanges has been the wild west. When Mt. Gox filed for bankruptcy in 2014, it said it had lost 850,000 coins worth more than $450 million. Another $70 million-odd was stolen in a hack of Bitfinex last year. The likes of Deribit and Bitmex have been offering bitcoin futures and options for some time, but major institutional investors are only going to participate if they think the clearing and settlement process is rock-solid and the exchange itself reliably solvent.Change on that front is imminent. The Chicago Board Options Exchange is planning to start offering cash-settled bitcoin futures by next April, CNBC reported last week. Trading platform LedgerX LLC last month won regulatory approval from the U.S. Commodity Futures Trading Commission to act as a clearing house for derivatives settled in digital currencies. The ability to short or take leveraged positions in digital currencies could open them to a far wider array of investors.

What, though, is the value of a digital currency? It's a fair question, but one that could equally be leveled at gold. Since Richard Nixon ended the fixed $35 an ounce convertibility of gold in 1971, its value has risen at times (the 1970s, the 2000s) and fallen at others. The best argument to justify investing in gold these days is not that it's an eternal "store of value" but that its very weirdness makes it special: According to modern portfolio theory, you should buy the shiny stuff not for its superior investment returns, but because it doesn't correlate much to other asset classes such as stocks, bonds and commodities.

What, though, is the value of a digital currency? It's a fair question, but one that could equally be leveled at gold. Since Richard Nixon ended the fixed $35 an ounce convertibility of gold in 1971, its value has risen at times (the 1970s, the 2000s) and fallen at others. The best argument to justify investing in gold these days is not that it's an eternal "store of value" but that its very weirdness makes it special: According to modern portfolio theory, you should buy the shiny stuff not for its superior investment returns, but because it doesn't correlate much to other asset classes such as stocks, bonds and commodities.

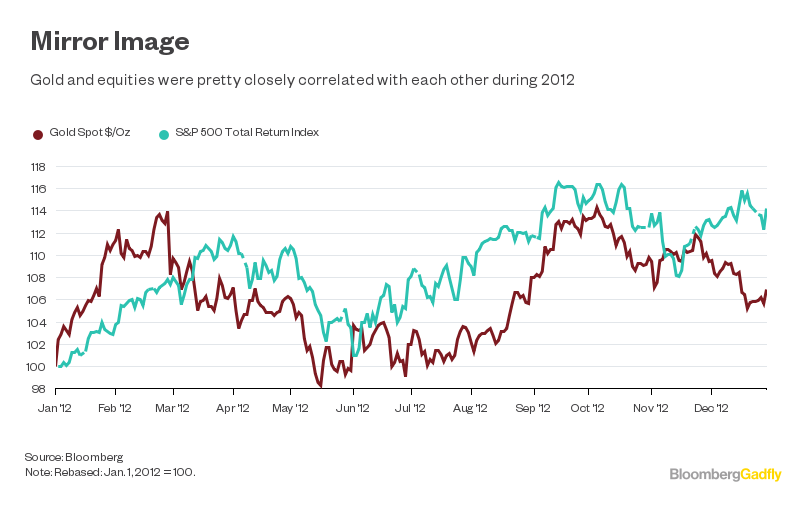

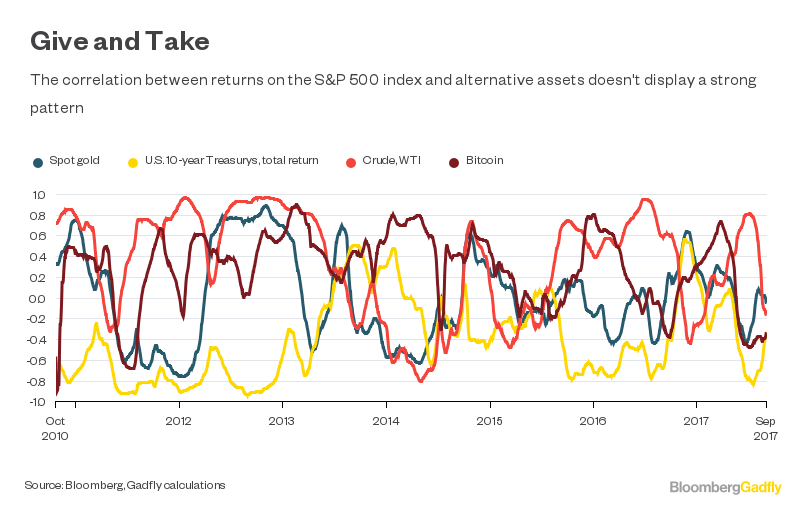

However, while gold did exhibit weak or negative correlations to returns on the S&P 500 for much of the 1980s and early 1990s, it's been positively correlated for extended periods since then. During gold's 2012 run-up, the two moved more or less in tandem. If gold deserves investment dollars because its inconsistent correlation with equities helps diversify portfolios, the same argument can be made for bitcoin, too.Digital currencies may be as vulgar as the original barbarous relic, but neither is going away any time soon. If that makes investors in both look less like seers and more like problem gamblers betting on where a fly will land — well, welcome to financial markets.

However, while gold did exhibit weak or negative correlations to returns on the S&P 500 for much of the 1980s and early 1990s, it's been positively correlated for extended periods since then. During gold's 2012 run-up, the two moved more or less in tandem. If gold deserves investment dollars because its inconsistent correlation with equities helps diversify portfolios, the same argument can be made for bitcoin, too.Digital currencies may be as vulgar as the original barbarous relic, but neither is going away any time soon. If that makes investors in both look less like seers and more like problem gamblers betting on where a fly will land — well, welcome to financial markets.

Author: David Fickling

Posted By David Ogden Entrepreneuer

Alan Zibluk – Markethive Founding Member